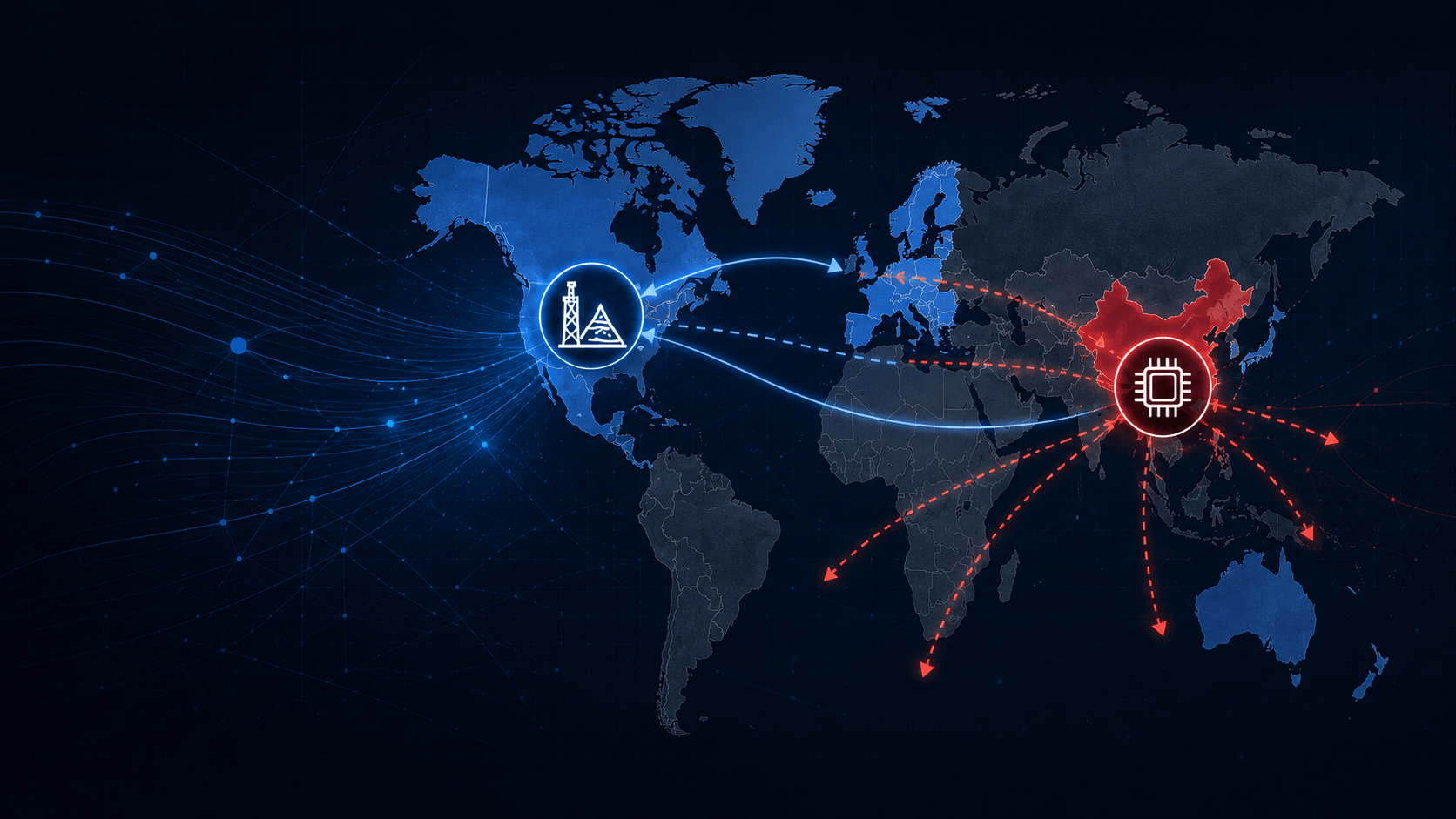

The AI race has moved into the supply chain.

The West holds the downstream chokepoints: U.S. chip design, Dutch lithography, German optics, and Taiwanese fabrication. These layers decide who can produce advanced chips at scale.

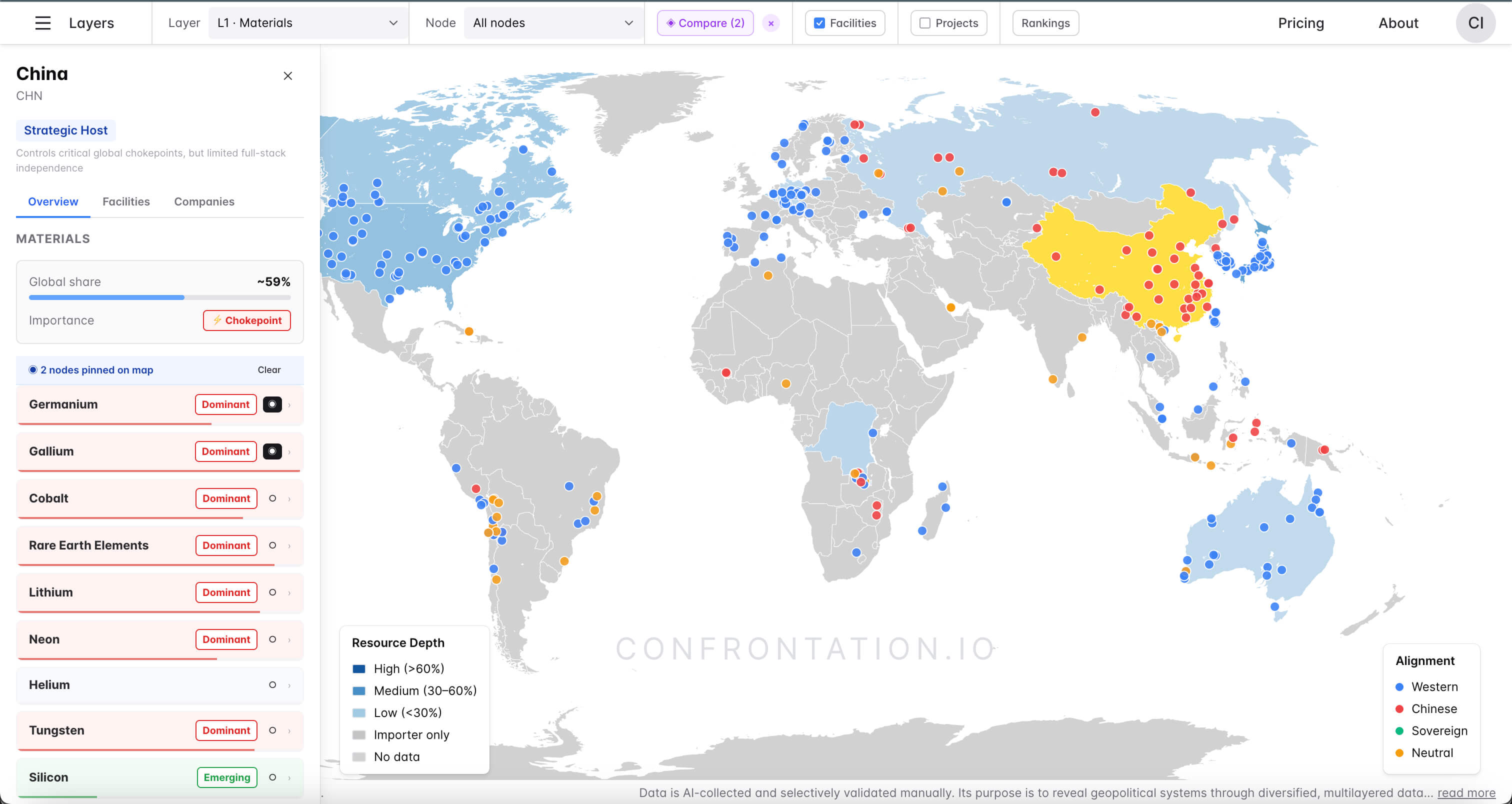

China holds leverage upstream. Gallium and germanium are small materials, but they sit inside the systems that connect, power, and support advanced computing. China controls the refining layer behind them.

This is why the conflict is becoming structural. The West is trying to block China from the machines needed to scale modern AI chips. China is using materials restrictions against the supply chains those machines depend on.

The race is no longer abstract. It is machine layer against materials layer.

Gallium, Germanium, and Lithography

To understand this part of the U.S.–China technology conflict, the stack has to be reduced to three pressure points: gallium, germanium, and lithography. Two are materials. One is a machine layer.

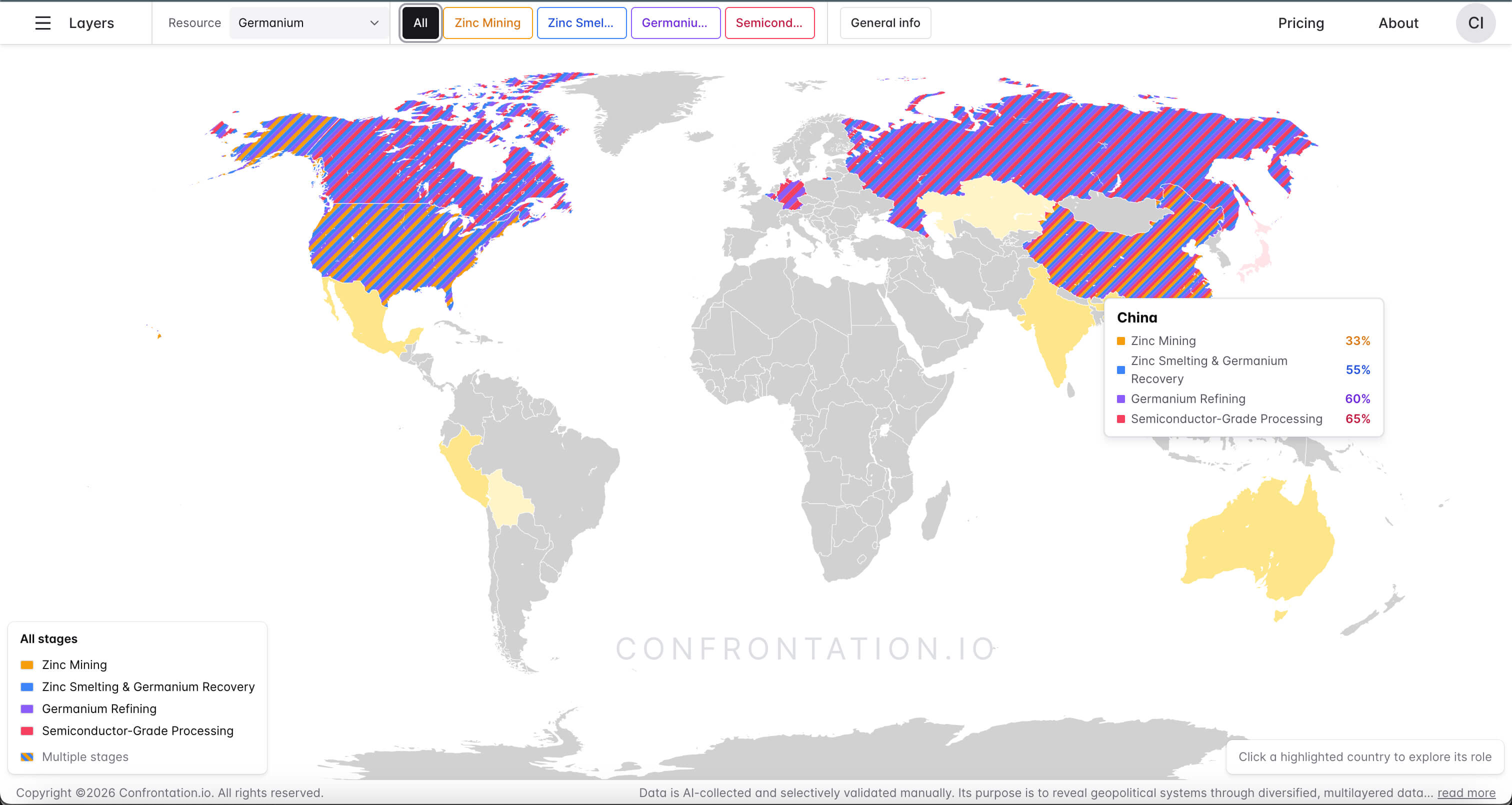

Gallium and germanium are not rare earths. They are mostly produced as byproducts from larger industrial processes: gallium from aluminum production, germanium from zinc refining and coal ash. Their strategic value comes from where they sit inside advanced infrastructure, not from their volume.

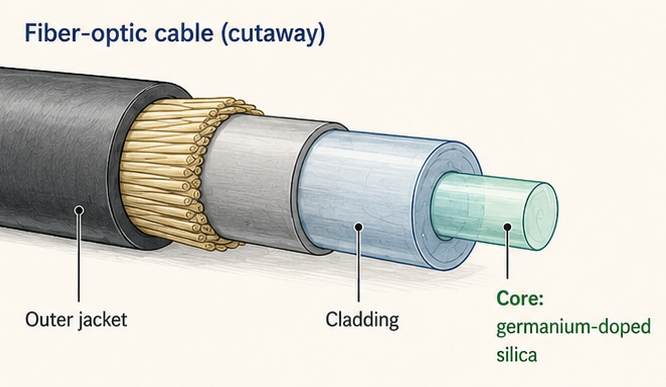

Germanium sits in the network layer. Modern AI training depends on huge numbers of GPUs moving data between each other at extremely high speed. The data center is not just a room full of chips; it is a communication system. Fiber-optic cables carry that traffic, and germanium is used in the glass core to help guide light through the fiber with low signal loss. It is part of the physical highway that lets AI systems move data at scale.

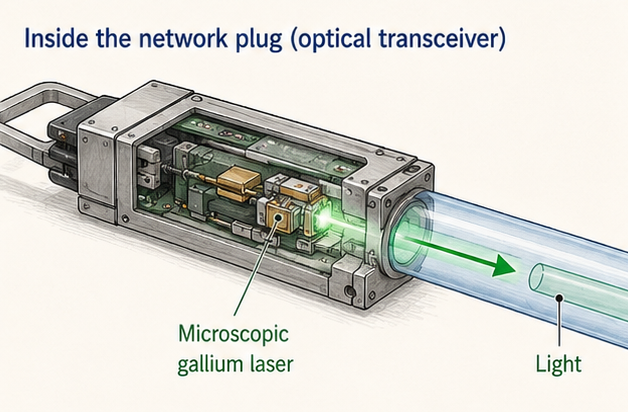

Gallium sits in the signal and power layer. Gallium-based compounds are used in the tiny lasers and optical components that push light into fiber networks. Gallium nitride is also used in high-efficiency power electronics, including server power systems that have to move large amounts of electricity with less heat and less wasted energy.

So the material logic is direct. Germanium helps carry the signal. Gallium helps generate and manage it.

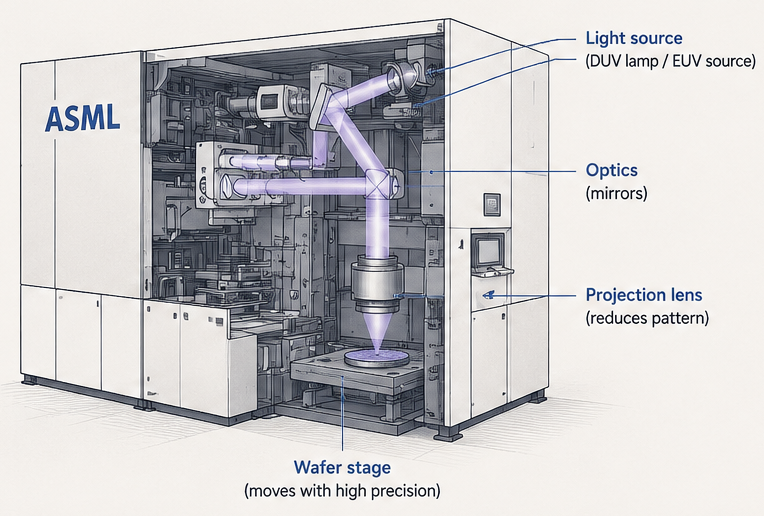

Lithography sits on the other side of the stack. It is the machine layer that turns chip designs into physical microchips. These systems project microscopic circuit patterns onto silicon wafers, allowing advanced chips to be manufactured at scale. The most important lithography machines come from ASML in the Netherlands, with critical optical systems from Germany.

This is the connection between the two sides of the conflict. China holds leverage in selected upstream materials. The West holds leverage in the machines needed to print advanced chips. Gallium and germanium expose the material dependency. Lithography exposes the machine dependency.

How China Built the Bottleneck

Today, China controls the overwhelming majority of global gallium production and a dominant share of germanium production. The exact numbers vary by source and year, but the structure is clear: most of the usable supply passes through Chinese industrial capacity before it enters the global technology chain.

Gallium is mainly recovered from bauxite and alumina production. Germanium is mainly recovered from zinc refining and coal ash. These are not simple mining stories. They are refinery stories. The country that controls the processing infrastructure controls the output.

This is also China’s hidden vulnerability. A large part of the raw feedstock behind these materials can come from outside China. In germanium, for example, zinc concentrates and related inputs can be sourced from countries such as Australia, Peru, Canada, and others. China’s strength is not full geological ownership. Its strength is the industrial system that separates, purifies, and scales these trace materials.

That system is difficult to replicate. Gallium and germanium extraction requires energy-heavy, chemically intensive processing connected to larger aluminum, zinc, and coal-based industrial chains. Over time, many Western countries allowed this capacity to shrink. High energy costs, environmental rules, low margins, and unstable prices made the business unattractive. China absorbed the dirty and low-margin part of the chain, then turned it into strategic leverage.

The pricing structure helped keep the bottleneck in place. When supply is available and cheap, new refineries are hard to justify. When supply becomes politically unstable, buyers want alternatives, but investors still face years of cost, permitting, and uncertain demand. China can keep the market open enough to prevent panic, but unstable enough to remind buyers who controls the gate.

After processing, the purified materials move downstream to advanced technology producers in Japan, South Korea, Europe, and the United States. Those firms convert them into optical components, wafers, compounds, sensors, and other high-tech inputs. China sits in the middle: not always at the final product layer, and not always at the raw material layer, but at the industrial bottleneck between them.

The Restriction Cycle

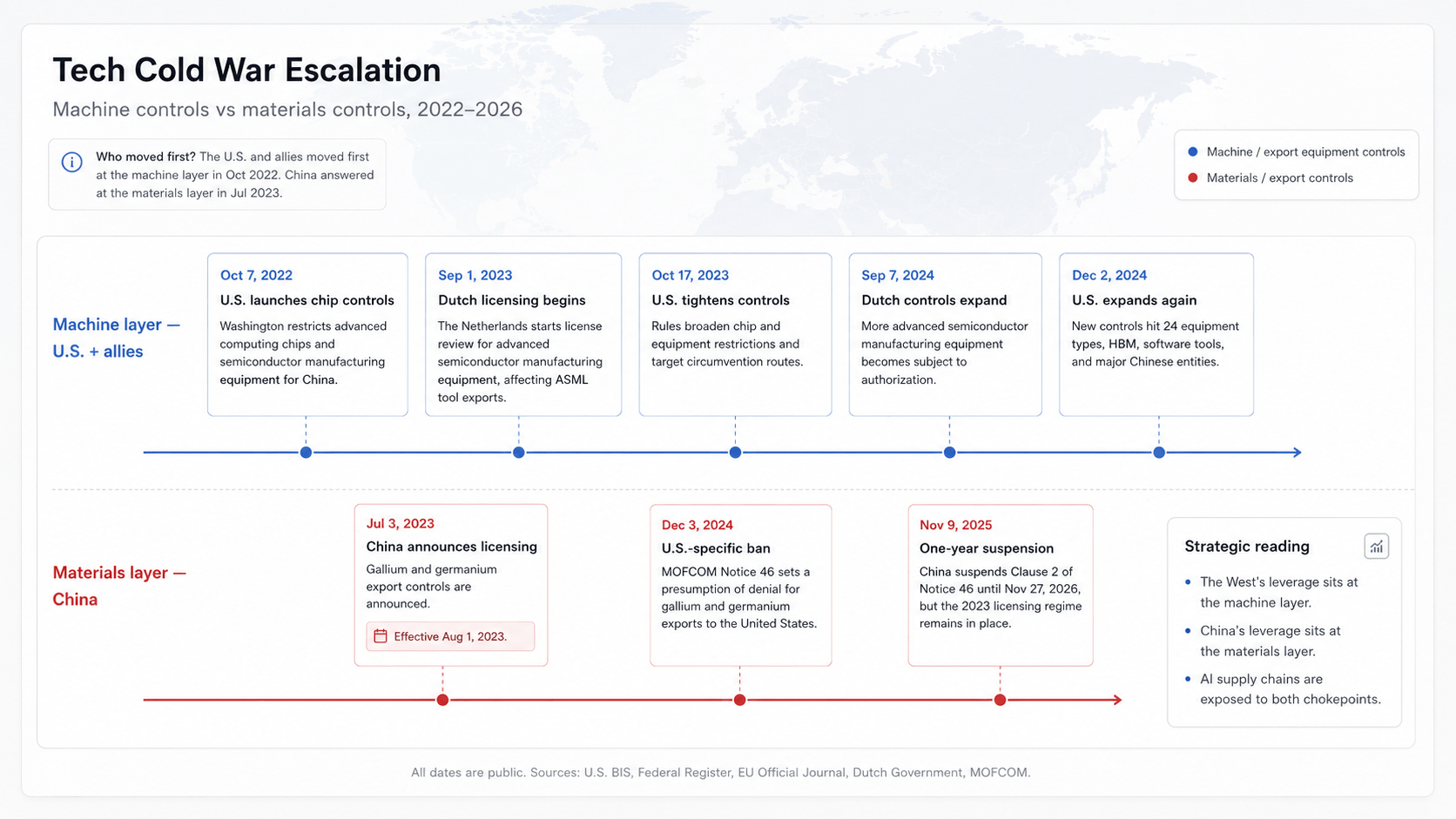

The conflict moved gradually through the stack.

In October 2022, the United States began restricting China’s access to advanced AI chips and semiconductor manufacturing equipment. The first pressure point was downstream: chips, tools, and the machine layer behind advanced fabrication.

In 2023, the pressure expanded to Europe. The Netherlands introduced export licensing for advanced semiconductor equipment, directly affecting ASML systems. The restriction was no longer only American. It reached the European machinery layer that China needed for advanced chip production.

China answered from the other side of the stack. In July 2023, Beijing announced export licensing requirements for gallium and germanium. The signal was clear: if the West used machine access as leverage, China could use material access as leverage.

By 2024, the structure hardened. Western restrictions on chipmaking tools expanded, while China moved beyond general licensing and introduced U.S.-specific restrictions on gallium and germanium exports. The conflict became more targeted. Machines were being blocked in one direction. Materials were being filtered in the other.

China still had a base to work from. Its fabs had already imported large numbers of ASML DUV machines before the controls tightened. That made the next phase less about starting from zero and more about extending the life of the existing fleet: upgrades, spare parts, secondary markets, older tools, and engineering workarounds.

In 2025, China temporarily suspended the U.S.-specific ban for one year, but the original licensing system stayed in place. The pressure did not disappear. It became conditional.

The result is an asymmetric restriction cycle. The West pressures China at the machine layer. China pressures the West at the materials layer. AI infrastructure sits between both chokepoints.

The impact is not immediate collapse. Data centers do not stop operating overnight because gallium or germanium exports slow down. The pressure works through uncertainty. Fiber optics, power electronics, defense sensors, chip materials, and server infrastructure all depend on supply chains where approvals can be delayed, end users can be exposed, and exports can be restricted case by case.

The Decoupling Race

The next phase is a race between two sovereignty projects. The West is trying to rebuild gallium and germanium supply chains outside China. China is trying to reduce its dependence on Western lithography and semiconductor equipment.

Both races point toward the same window: 2028 to 2030. By then, the question is whether the West has enough non-Chinese material capacity, and whether China has enough domestic machine capacity.